jtr1962

Storage? I am Storage!

If this interrupts production and supply chains, a lot of Americans might know the feeling of hunger for the first time in their lives. Then again, collectively we can all afford to lose a good amount of weight.

www.theguardian.com

www.theguardian.com

The German health ministry spokesperson declined the opportunity to correct any inaccuracies in Die Welt’s account.

Keep pushing the fake news. That story has already fallen apart.This is a new low for the administration and that's saying a lot.

Trump 'offers large sums' for exclusive US access to coronavirus vaccine

German government tries to fight off aggressive takeover bid by US, say reports

Nothing has fallen apart yet. I'm not seeing a credible source from your point of view. Grenell is a Trump loyalist...so no thanks, can't trust a Trump crony.Keep pushing the fake news. That story has already fallen apart.

I doubt we could be that lucky for them to go out of business. I haven't even connected my home phone in the year I've been at my new place. I can see in the online records it gets tons of calls.Amazing in all this that I'm still getting telemarketing calls (which I never answer of course). If there's any silver lining to this, it could be that it lasts long enough to put most of these telescammers out of business for good.

www.theatlantic.com

www.theatlantic.com

www.npr.org

www.npr.org

thehill.com

thehill.com

I think it's a good idea but at the same time we should make sure that people who already have money coming to them don't have it seized. I'm talking specifically about people who have tax offsets because they owe on student loans. The government should suspend these tax offsets so these people can spend their refunds instead and help the economy.So now everyone is Andrew Yang and wants to throw out money. Maybe Trump will announce that Bank of America will send the money quickly and they've worked something out. BoA will reply in a surprised tweet...we're doing wut now?

Caller ID verification may well be a game changer as more phone providers roll it out.I doubt we could be that lucky for them to go out of business. I haven't even connected my home phone in the year I've been at my new place. I can see in the online records it gets tons of calls.

I think you might need help... A denial directly from the company isn't good enough, but you'll believe an anonymous report from fake news specialists with no credibility while other media outlets are surreptitiously walking back their reports by watering down the initial claims.Nothing has fallen apart yet. I'm not seeing a credible source from your point of view. Grenell is a Trump loyalist...so no thanks, can't trust a Trump crony.

Second...Trump is the largest proponent of fake and misleading news daily...right from his own mouth but you're ok with that. Why should I trust your source?

Can't do it without changing federal law and amending the constitution. So, no it won't happen.Anyone else thinking that if large numbers of people aren't vaccinated by November that we should just postpone the election until 2021?

Amazing in all this that I'm still getting telemarketing calls (which I never answer of course). If there's any silver lining to this, it could be that it lasts long enough to put most of these telescammers out of business for good.

I doubt we could be that lucky for them to go out of business. I haven't even connected my home phone in the year I've been at my new place. I can see in the online records it gets tons of calls.

(what happened to the head scratch emoticon?)

(what happened to the head scratch emoticon?)Have all the banks and corporations been given their free money yet? Because we all know they come first. And second. And thrid. Fourth, fifth. etc. Maybe the lil guy is 9th on the list.So now everyone is Andrew Yang and wants to throw out money. Maybe Trump will announce that Bank of America will send the money quickly and they've worked something out. BoA will reply in a surprised tweet...we're doing wut now?

The student loan messes needs work. I agree. And screwing over banks to help the little guy sounds really appealing. Fuck the banks. But just canceling "large swath of student loans" sends the wrong message. So no. I worked tons of OT, nearly a whole year, and lived on "bread & water" to save enough to pay off my student loan. It was tiny by today's standards (under $20k total, final lump payment was just under $10k) but I took responsibility for my actions (wasting time/money at uni) and paid my debts.And as I said earlier, the government should seriously consider canceling a large swath of student loans, starting with the oldest loans first. You want a stimulus? I can't think of anything better. This is trickle up economics at its finest. That money will be pumped right back into the economy.

Caller ID verification may well be a game changer as more phone providers roll it out.

Anyone else thinking that if large numbers of people aren't vaccinated by November that we should just postpone the election until 2021?

Ah smooth...you edited you post to add the CureVac tweet after the fact. What kind of help do you think I need?I think you might need help... A denial directly from the company isn't good enough, but you'll believe an anonymous report from fake news specialists with no credibility while other media outlets are surreptitiously walking back their reports by watering down the initial claims.

Telemarketers will be the second to last thing to perish on this planet. The first being cockroaches.

You are paying for a landline that's you don't have a phone on? Part of a "internet/tv/phone bundle" you can't, or not worth it to, cancel/seperate? I gave my Ooma "landline" number to 4 family members that I'd take a call from. And I only call them with that number. I don't call anybody outside that circle with that number. Have never received telemarketing calls.

Slow your roll. I didn't add it after your reply. At best I added it at the same time as your reply. None of which changes that the story you posted as proof of the depravity of Trump and his administration is still just as fake and was just as debunked as it was before you posted it.Ah smooth...you edited you post to add the CureVac tweet after the fact. What kind of help do you think I need?

Loans more than 20 years old should be cancelled. Here's why. Starting a while back, maybe during the Obama administration, new student loans had two things older ones didn't. First, they had what was called income-based repayment. This means your payments were capped at some reasonable percentage of your disposable income regardless of how much you owed. I think if you made under the poverty line, your payments were zero. Second, after 20 years any remaining balance on the loan was forgiven. Therefore, to treat older loans the same any loan older than 20 years should be cancelled.The student loan messes needs work. I agree. And screwing over banks to help the little guy sounds really appealing. Fuck the banks. But just canceling "large swath of student loans" sends the wrong message. So no. I worked tons of OT, nearly a whole year, and lived on "bread & water" to save enough to pay off my student loan. It was tiny by today's standards (under $20k total, final lump payment was just under $10k) but I took responsibility for my actions (wasting time/money at uni) and paid my debts.

And that's another problem similar to the one I just mentioned. ALL my promissory notes have collection fees capped at 25% of the original principal but that didn't stop them from adding fees above and beyond that, and then recategorizing the fees already added as "interest". I'm sure this is 100% illegal but they did it anyway. This is part of the problem. The majority of people who supposedly still owe money already made more than enough payments to pay off their loans if the payments were applied as they are with other types of debt (i.e. part goes to interest and part to principal). Instead, they apply the payments in the least favorable way. First they go towards outstanding interest. Once that's paid off they go towards outstanding collection fees. Only once there's no outstanding interest and collection fees do some of the payments go towards principal, with the rest going towards whatever interest was added that month.What needs to be done is the gov't needs to put up a big middle finger to the scummy banks and private lenders that went ape shit with interest and MORE IMPORTANTLY EXPENSES, FEES, PENALTIES, ETC. People are crapping their pants about the guy "profiteering on hand wipes and sanitizers" yet these scummy lenders cause a $10-20k loan to balloon up to $200-300k due to missed payments and default.

So if you're unable to get a job out of college and default because of it, you should be penalized? That's making an already difficult situation even worse. The only people who maybe we should penalize with collection fees are those who have the ability to pay but decided not to.Now if you did default, you should be punished and pay SOME fees and penalties but you shouldn't be, and Merc used to say, "anally chainsaw raped" because of it.

Here's my idea:1) Cap the stupid shit from happening. 2) Eliminate all the bullshit fees/penalties. Return your balance to a sensible number. I don't know the number but a percentage of the principle, NOT multiples of the principle. 3) Create a real consolidation repayment structure that enables people to realistically give them the ability to pay back their loan. 4) Allow for generous deferments for those in true need. 5) Allow for bankruptcy after 15, 20, 25 or however many years.

Do this but instead replace loans with grants. I agree we shouldn't give people large sums of money if they're poor students or want to study fields with poor prospects for getting a job. However, if they're smart and getting a useful degree, we should be willing to foot the bill for them, contingent upon their keeping up a certain GPA. Nobody should start off their working life with a huge loan balance.And most importantly, CUT OFF THE FREE MONEY TO EVERY DUMBFUCK WHO WANTS TO GO TO COLLEGE. I don't know a perfectly fair way to do this, but perhaps your total loan amount tied to your ability, grades, SAT scores, etc. Einstein in high school, you can borrow $200k, 2.7 gpa and 1000 total SAT score = $15k loan. 1.7 gpa and 700 SAT score = jr college. Maybe set aside a good portion of loan money for NON-COLLEGE trade schools.

Free money = explosion in costs because, hey free money = "A $280k Harvard degree in 'horse-shit' studies. = High debts = hElP Me i caNnOT pAy mY LoAN bACk.

Then they shouldn't take out a huge loan to pay for their "education". This isn't hard.Nobody should start off their working life with a huge loan balance.

mobile.abc.net.au

mobile.abc.net.au

You're forgetting that lots of types of degrees benefit more than just the person getting them. Doesn't having more engineers, doctors, and scientists benefit society at large? And society also benefits from the higher taxes someone who realized their potential will pay over their working lives. Telling people they can go to school only if they're willing to go into hock sends a very wrong message. If a person has potential, that person is worth investing in via grants. If they don't want to invest in you, then my attitude is once you're making the big bucks the tax man shouldn't have his hand out. That seems fair. If you have to borrow your way through school, you get a lifetime exemption from income and sales taxes since the government felt you weren't worth investing in. What otherwise would have gone towards taxes can go towards repaying your loans.If you want something that has value (college degree) you need to pay for it. With your own money or money you borrow. If you borrow money you should have to pay it back with some benefit (interest) for the lender. With student loans, I'm OK with "extra or special" protections being put into place so that new borrowers/students don't destroy their future either through their own incompetence or through malfeasance of lenders.

It's pretty much a matter of semantics because if student loan balances were recalculated based on a reasonable interest rates and applying payments to principal first most loans would be gone. The only difference is they would be paid off fair and square, versus forgiven. If my loan was given the treatment I mentioned above, I would be due a refund of over $2,000 plus whatever interest they chose to give me on overpayments. And given the disparity in treatment between older and newer loans, which are forgiven automatically after 20 years, applying those terms to all loans essentially means loans over 20 years old would be gone regardless of how much was paid towards them.Maybe it's just semantics (cancel debt vs fairly recalculating debt) but simply allowing people a free pass for their irresponsibility is wrong. Many, many people would not have defaulted or been buried under impossible debt if all the current horseshit and retroactive fuckery didn't take place.

You can do this with grants. Here's my idea. You give grants for education instead of loans, but limit those to some reasonable number, like maybe $10K to $15K annually. Any school that agrees to take students getting grants also agrees to not charge that student anything. They would have to accept the grant to pay for 100% of tuition, room, and board. The only way a school could charge more would be to not accept any government grants, and rely 100% on payments from students, their parents, and private endowment funds. Those schools could charge whatever they want, but at least what they could charge would be inherently limited by what the sources of income I mentioned were able to pay.I prefer loans to qualified students over grants. Sensible loans, not the horseshit mess we have now. My #4 point of allowing for sensible deferment would solve the problem of a newly graduated student that could not immediately find a job, or a job with a high enough pay.

Private grants are fine for those that want to give them. And a limited amount of federal grants to those extraordinary kids from the lower socioeconomic classes is warranted. Stop the free money. Eliminate most of the loan guarantees so banks will lose if they haphazardly give away money like candy. This will cut back supply. Colleges will be forced to lower costs. etc.

We need to reverse the upward spiral of costs.

The problem is the system feeds on itself. Years of government throwing money at the problem means it's no longer possible to work your way through school by waiting tables or something similar.Then they shouldn't take out a huge loan to pay for their "education". This isn't hard.

See my response to snowhiker above. We first fix existing debt by recalculating balances as I described. Many loans will be repaid fair and square if that's done. If some people still owe money, it will be a much smaller, more manageable amount, and we can probably get them to pay most of it.The problem doesn't need more gov't intervention in the student loan market to fix it, it needs the gov't taken out of the student loan business. The cost of college has spiraled out of control because there's a near unlimited supply of money for schools to suck up because the lender (gov't) doesn't care about your ability to repay it. They'll effectively loan you however much money you want regardless of how invaluable the degree you're buying is and your likely inability to make good on the loan. Colleges are businesses, not institutions of learning. They're busy competing with one another not over who can educate their students the best or guarantee the highest salaries for their graduates with a particular degree, but who has the most resort like accommodations for the students since they're selling you a multiyear lifestyle with a piece of paper at the end.

If the lender had a vested interest in getting repaid this would all stop. Many, perhaps most, people wouldn't be able to get loans to cover their current degrees because the lender would decide the risk on the loan is too high. Once the money train stops, colleges will have to adjust prices to what people can afford to pay and compete on what value they're offering for the cost. There'd be a rough few years of transition in there, but it would all work out.

No argument there but I mentioned that cancelling or otherwise readjusting student loan balances will likely eventually be needed as part of the stimulus. There are only so many other levers we can pull, like giving cash directly to people. We need to go big, and we need to do it soon:Regardless, we've got far bigger and more pressing problems than student loans right now.

Just revisiting this 6 days later. Right now we're under 19,000 and I don't think the blood bath is anywhere near over. I wouldn't be surprised if we bottom out at under 10K, although the market will likely quickly rebound to at least 20K once this is over.Tangentially related...since the DJI & S&P is down a bunch more...is it time to buy yet, or wait for ~19000?

I saw...my cash is still sitting in at my broker waiting to pull the trigger on some investments when I feel like the time is right. I don't know if it will go as low or below 10K...that's pretty serious, but maybe? I also don't think we're done heading down. The Dow has now gone below when Trump took office. Hopefully he takes responsibility for the losses just as much as he takes credit for the gains (unlikely). His administration has failed at a proper response and management to this epidemic so he should get that credit just like he would blame any former administration. I can't wait to yet again spend my tax money bailing out airlines/banks/etc that didn't plan for a rainy day like everyone else preaches US citizens should be doing.Just revisiting this 6 days later. Right now we're under 19,000 and I don't think the blood bath is anywhere near over. I wouldn't be surprised if we bottom out at under 10K, although the market will likely quickly rebound to at least 20K once this is over.

Well, I still have the savings bonds from my father to invest, and I could invest some more from my savings account when I think the time is right. I think we're going down to at least 15K. So does this guy. A lot of what happens depends upon the stimulus package(s) and what happens with the virus. Things like this can and have just suddenly died off on their own. There's some talk warmer weather might slow it.I saw...my cash is still sitting in at my broker waiting to pull the trigger on some investments when I feel like the time is right. I don't know if it will go as low or below 10K...that's pretty serious, but maybe? I also don't think we're done heading down. The Dow has now gone below when Trump took office. Hopefully he takes responsibility for the losses just as much as he takes credit for the gains (unlikely). His administration has failed at a proper response and management to this epidemic so he should get that credit just like he would blame any former administration. I can't wait to yet again spend my tax money bailing out airlines/banks/etc that didn't plan for a rainy day like everyone else preaches US citizens should be doing.

No kidding. That's why we need to get a handle on this soon. In my opinion the impact on the economy can potentially be much greater than the impact of the pandemic itself. What's not helping is that governments, and many individuals, have zero cash reserve. If people lose their jobs, they're in deep shit. If they had 6 months or a year of savings, then can continue to spend and help the economy until this passes.There's no bottom to the stock market. We're on the brink of all the worldwide financial markets collapsing.

Is there any major gov't in the world that isn't seriously drowning in debt?No kidding. That's why we need to get a handle on this soon. In my opinion the impact on the economy can potentially be much greater than the impact of the pandemic itself. What's not helping is that governments, and many individuals, have zero cash reserve. If people lose their jobs, they're in deep shit. If they had 6 months or a year of savings, then can continue to spend and help the economy until this passes.

China seems to have put a lid on it as well, at least if you can trust their data. There's only been a trickle of new cases for a while now. Unfortunately, they didn't seem to learn their lesson with wet markets. If they had shut those down for good after SARS we may never have seen this pandemic. Hopefully this time around they'll shutter these markets for good.Is there any major gov't in the world that isn't seriously drowning in debt?

The US and Europe didn't taken any lessons to heart from the close call the world has with SARS. Some asian countries like Taiwan, Singapore, etc. did which is why they seem to have been able to put the lid on the Wuhan Flu in comparison.

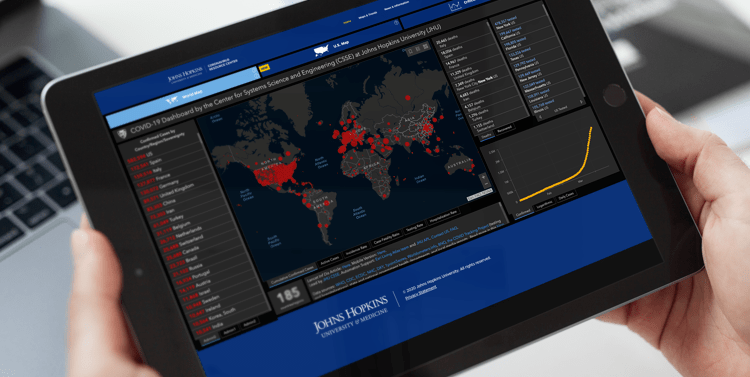

coronavirus.jhu.edu

coronavirus.jhu.edu

If you look at on a logarithmic scale the growth is already leveling out. Doubtless there are lots of people who got it before we implemented emergency measures, and will later be added to the case count, but I think the growth is going to top out within a few weeks, provided we don't relax restrictions or get complacent.COVID-19 Map - Johns Hopkins Coronavirus Resource Center

Coronavirus COVID-19 Global Cases by the Center for Systems Science and Engineering (CSSE) at Johns Hopkins University (JHU)

Total confirmed cases was just under 200k (198k'ish) earlier this A.M. Now it's at 215k. Maximize the bottom-right panel. The exponential growth does not look good. HOPEFULLY growth will level out like China's growth has the last month.

Two reasons for that. One is the largest percentage of elderly population outside of Japan. Two is their hospitals got overwhelmed. It seems with proper support care the overall mortality rate for this is under 2%, and may be a lot lower since undoubtedly we're still undercounting the number of cases. Without proper care we might be looking at a 10% mortality rate. Yet another reason to flatten the curve so large numbers of people don't get sick at once.Italy (pop. 60m), a country with less than 1/20 the population of China (1.42b) has nearly as many deaths! Fuck.

Because everyone there already died from it? Seriously, my best guess is they're being hammered by it but of course to keep their propaganda alive that they're the best country on Earth they're not releasing any figures. Think about it. The population is undernourished and disease-prone to start with. They don't have a great medical system. That's a perfect storm for an epidemic. I wouldn't be surprised if their death toll is already well into the 6 figures.Out of interest, I can't see to find any numbers from DPRK (North Korea)?

www.techtimes.com

www.techtimes.com